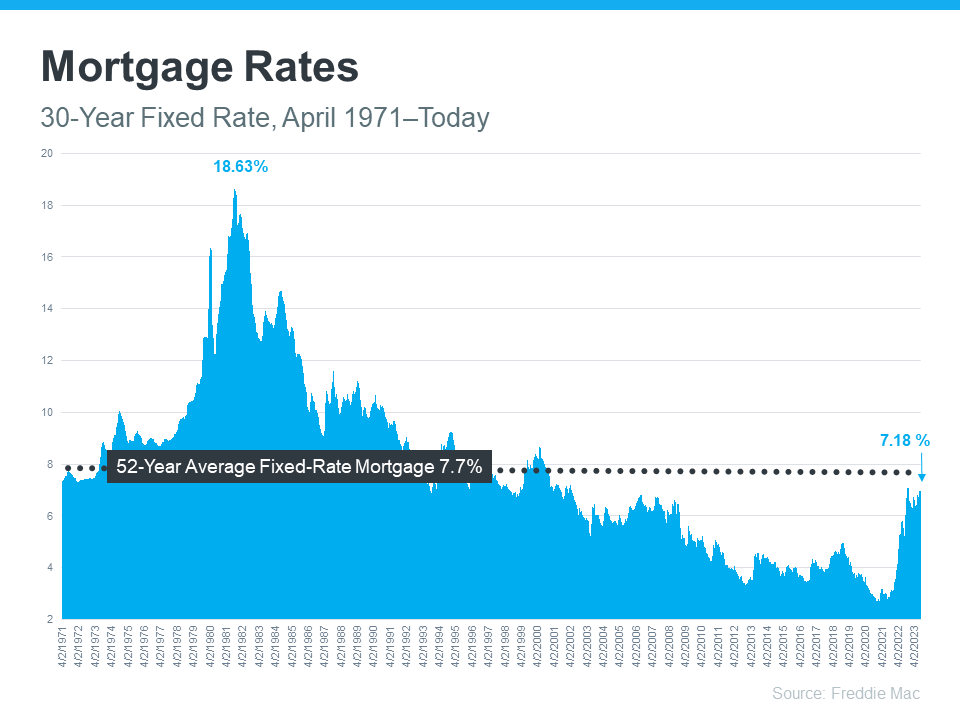

| If you’re hoping to buy a home this year, you’re probably paying close attention to mortgage rates. Since mortgage rates impact what you can afford when you take out a home loan – and affordability is a challenge today – it’s a good time to look at the big picture of where mortgage rates have been historically compared to where they are now. Beyond that, it’s important to understand their relationship with inflation for insights into where mortgage rates might go in the near future. A Bit of Context to the Sticker Shock Freddie Mac has been tracking the 30-year fixed mortgage rate since April of 1971. Every week, they release the results of their Primary Mortgage Market Survey, which averages mortgage application data from lenders across the country (see graph below): |

Looking at the right side of the graph, mortgage rates have increased significantly since the start of last year. But even with that rise, today’s rates are still below the 52-year average. While that historical perspective is good context, buyers have gotten used to mortgage rates between 3% and 5%, which is where they’ve been over the past 15 years.

That’s important because it explains why the recent jump in rates might have you feeling sticker shock even though they’re close to their long-term average. While many buyers have adjusted to the elevated rates over the past year, a slightly lower rate would be a welcome sight. To determine if that’s a realistic possibility, it’s important to look at inflation.

Where Could Mortgage Rates Go in the Future?

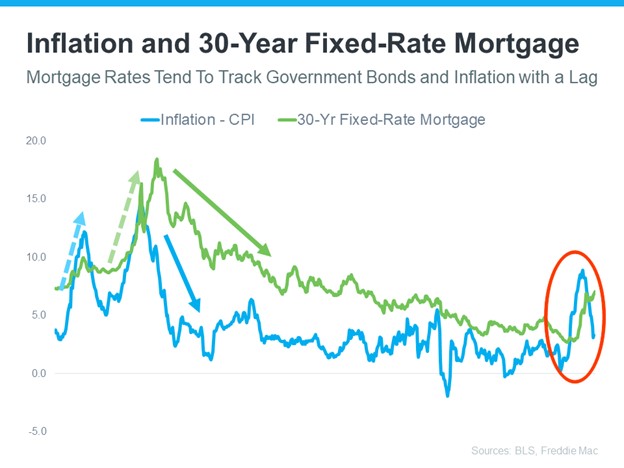

The Federal Reserve has been working hard to lower inflation since early 2022. That’s significant because, historically, there’s been a connection between inflation and mortgage rates (see graph below):

This graph shows a pretty reliable relationship between inflation and mortgage rates. Looking at the left side of the graph, each time inflation moves significantly (shown in blue), mortgage rates follow suit shortly after (shown in green). The circled portion of the graph points out the most recent spike in inflation, with mortgage rates following closely behind. As inflation has moderated a bit this year, mortgage rates haven’t yet made a similar move. That means, if history is any guide, the market is waiting for mortgage rates to follow inflation and head back down (WOOHOO!). It’s impossible to accurately predict where mortgage rates will go for sure, but moderating inflation means mortgage rates going down in the near future would fit a well-established trend.

KEY TAKEAWAY

To understand where mortgage rates may be going, it’s helpful to look at where they’ve been in the past. There’s a clear connection between inflation and mortgage rates, and if that historical relationship holds true, the recent decline in inflation may mean good news for the future of mortgage rates and your homeownership goals. Call me to discuss your real estate goals. Lets make them a reality!

Home Prices Are Still Climbing

This year is winding down. If you’re considering buying a home or selling your current one to find something that better suits your needs, you may have questions about what’s happening with home prices in todays market. Here’s what you need to know.

There’s a lot of chatter and misinformation out there, but no matter what you may have heard, the national research shows prices have actually been climbing again (see graphs below):

As you can see, in the first half of 2022, home prices went way up. Those increases were dramatic and unsustainable. So, in the second half of 2022, prices adjusted. The dips were small and didn’t last very long.

But what’s important to know is that, in 2023, prices are going up again, and this time it’s at a more normal pace. All three reports now show more typical price increases this year, which is good news for the housing market.

After seeing steady home price growth at the national level for the last several months, you may wonder if prices are going up in our (NYC metro & surrounding suburbs) area, too. Know this: home prices are appreciating in our area.

Many experts are forecasting that home prices will end the year in the positive and continue going up in 2024.

Here’s How This Affects You

- For Buyers: If you’ve been waiting to buy a home because you were concerned it might lose value, the fact that home prices are going up should ease your worries. Buying a home before prices climb higher can be a smart move since home values typically appreciate over time.

- For Sellers: If you’ve been postponing selling your house because you were worried about how changing home prices would affect its value, now might be a good time to work with a realtor (ME) to put your house on the market. You don’t have to wait any longer because the data shows home prices are in your favor.

KEY TAKEAWAY

If you delayed moving because you were concerned home prices would drop, don’t worry – the numbers show they’re going up nationally. To better understand how home prices are changing in your local neighborhood or county, let’s connect.